The Australian road transport industry is not outside the influence of the Australian economy, suffering the ‘slings and arrows’ of the greater economic picture. The last quarter of a century reveals some important parameters that are both critical to operators, ancillary fleets and even to policy makers themselves.

The total proper road task should be measured in gross tonne kilometres (gtkms) as even empty trucks, or just their tare weights, do a modicum of road damage.

But more often than not the road task is measured as a nett tonne kilometre task, which many economists subscribe to.

Even rail pricing is based on gtkms as it is recognised that empty trains do track damage, so why not measure the road sector in the same way?

Total gross tonne kilometre road task

Although data is limited to almost the last 20 years, there have been some surprising consistencies over the 1998-2016 period for the road transport task.

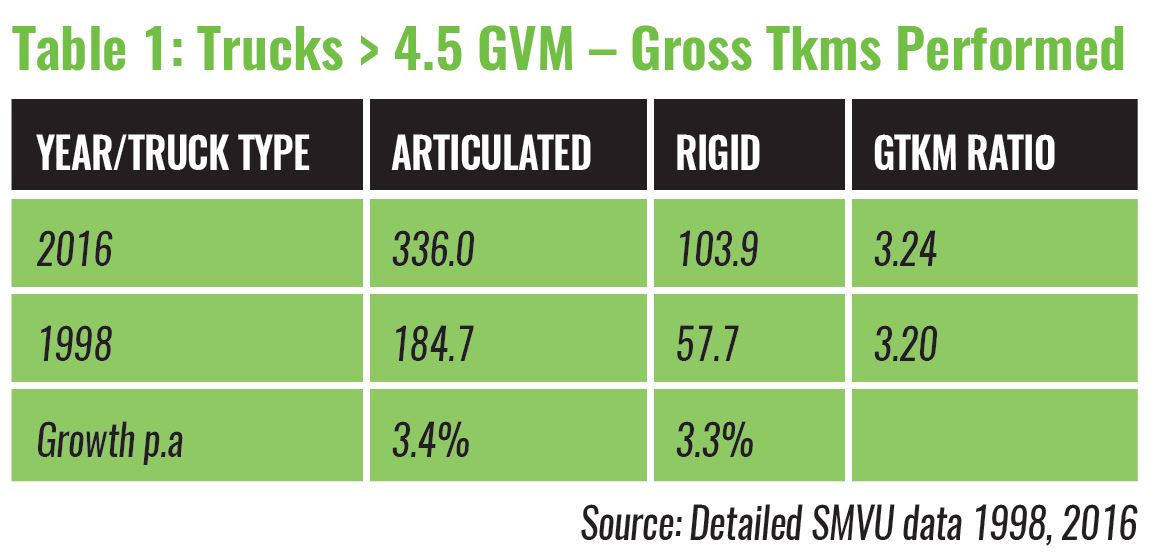

Firstly, despite some hiccups both rigid and articulated truck gross tonne kilometres have had growth of around 3.4 per cent per annum over that period (see Table 1).

What is surprising is that despite the e-commerce boom the ratio of task delivered by articulated and rigid trucks has stayed relatively consistent at a ratio of 3.2 when the articulated task is compared to the rigid truck task over that period.

This is a very interesting task growth observation.

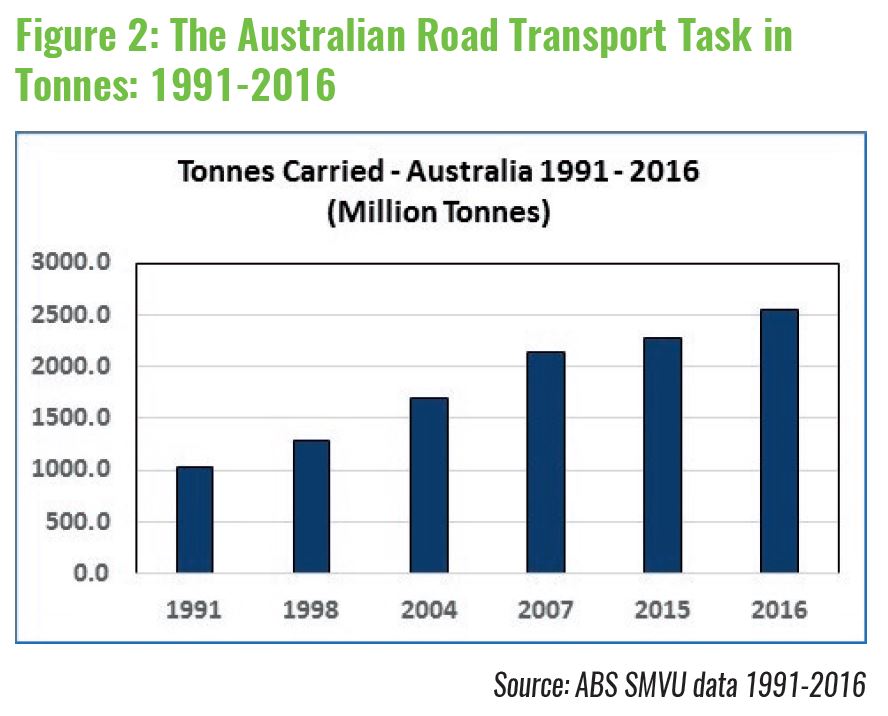

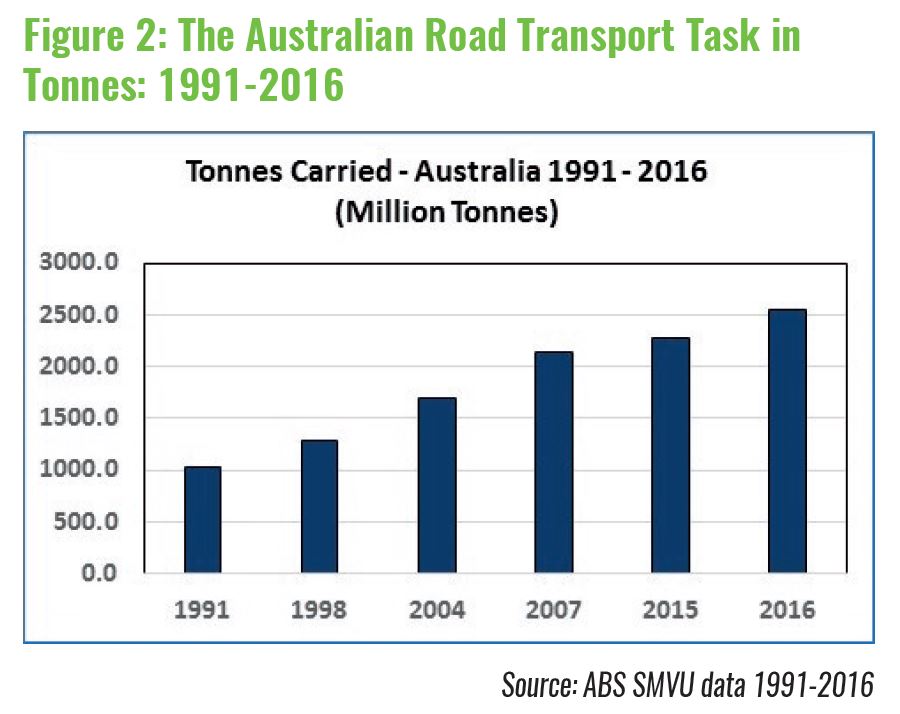

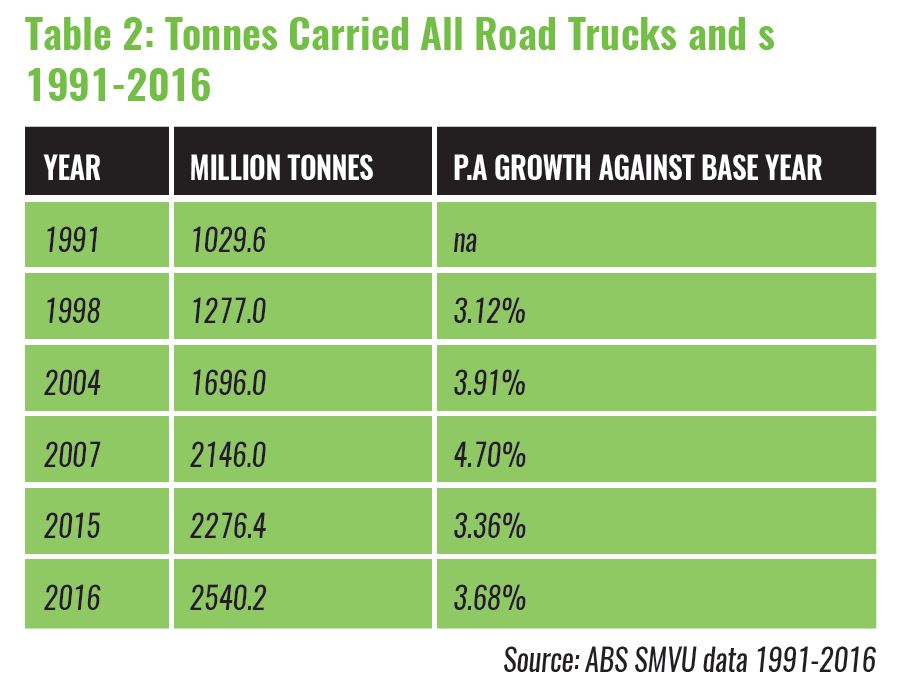

The Total Tonnes Carried in Australia 1991-2016

Over the 25 years to 2016 the total Australian Road Freight task increased by 146 per cent (a factor of 2.46) since the 1991 recession year.

These figures presented in Table 2 reflect both the combined total truck and LCV tonnages carried in Australia over that period.

Overall, since 1991 the average compounding rate of tonnage growth for the Australian road task has been nearly 3.7 per cent per annum across all commodities.

The rate of growth up to the 2007 Global Financial Crisis was 4.7 per cent compounding per annum.

Between 2007 and 2015 the growth rate was only 0.74 per cent per annum over that eight year period and this weakness has also been reflected in the tight economic times for operators over this time period.

Who makes up the Australian road sector?

Possibly the least known about the Australian trucking population is who actually carries what.

In Australia, as in all countries, there are the carriers that do transport for money, hire and reward carriers, and others that carry their own goods as part of their operation.

These operators are known as ancillary operators, sometimes called ‘own account’ operators.

Examples of these operators are farmers, small retailers, small manufacturers, some government agencies, and local governments that do not outsource their operations to say a third party logistic provider but do the cartage themselves.

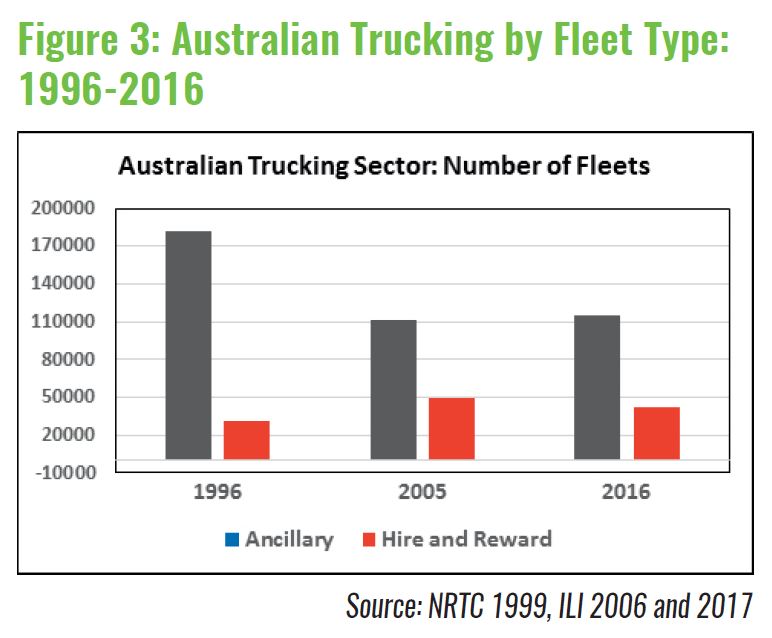

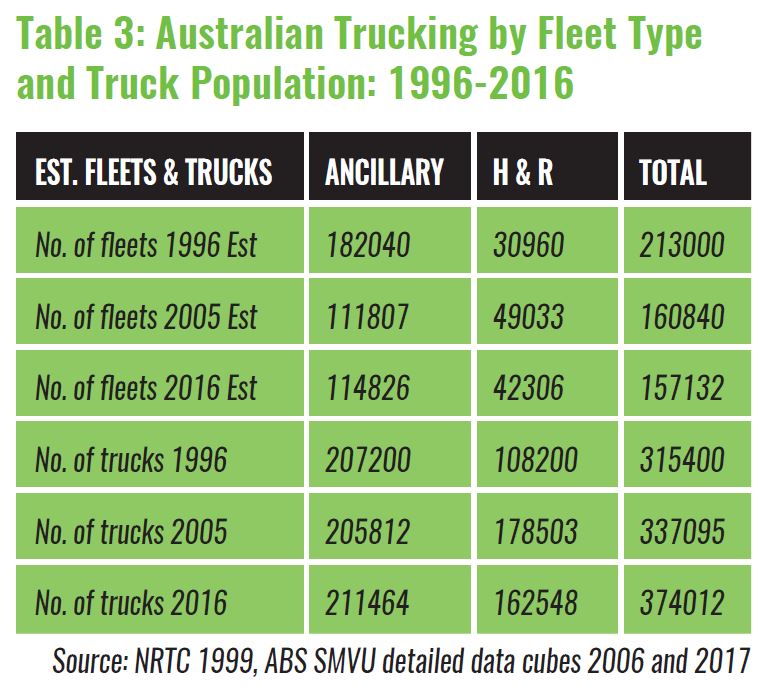

Table 3 reflects the balance between the hire and reward (H&R) and ancillary fleets and vehicle numbers for trucks greater than 4.5 tonnes GVM over the last 20 years.

Roughly the ratio of trucking fleets in Australia has ranged from six times more ancillary fleets in 1996 when compared the H&R fleet numbers.

Of recent years this ancillary ratio has dropped to 3.5 times the fleet numbers in the H&R sector.

The size of the ancillary sector often comes as a surprise to regulators who often only survey operations and the performance of the H&R sector.

Currently Australia has little data on the maintenance, fatigue performance, and even kilometre performance of the ancillary sector.

Fatigue researchers have also often just relied on telephone lists and association data to do fatigue surveys which obviously restricts the analysis to the H&R sector only.

It was only in 2015 that Australia had its first snapshot of the driver fatalities in the ancillary sector, and yet we continually examine only the behaviour of the H&R sector through on road enforcement findings and yet more H&R fatigue studies that are said to reflect the ‘whole industry’.

Many researchers do not know what the ancillary sector is and even state freight flows are often estimated by interviewing road transport association members without talking to any ancillary fleets.

It is somewhat a worry that the ancillary sector has come under such little scrutiny.

Most road transport associations are comprised of the H&R sector and possibly with the exception of the Farmers’ Federations, the ancillary sector is rarely canvassed with regard policy issues.

The numbers of trucks in the ancillary sector has remained steady over the last 20 years, with a population of slightly over 200,000 vehicles.

The H&R vehicle numbers have grown from some 108,000 in 1996 to 162,000 in 2016 reflecting significant outsourcing to the H&R sector.

Within this H&R sector, however, the configurations have evolved somewhat, especially as B-doubles and even Performance Based Standard vehicles have emerged strongly over this period.

The B-doubles, which began to grow from the mid-1980s, have now reached a population of some 19,000 vehicles, and PBS vehicles, which first emerged in 1997/1998, have hit a current level of some 5,000 vehicles.

The decline in the 2016 number of H&R fleets, however, has been primarily driven by the fall in owner-driver numbers, estimated by one agency to be down by some 44 per cent since 2010, as well as significant consolidation within the larger fleets due to a decade of poor economic conditions for this H&R operator sector.

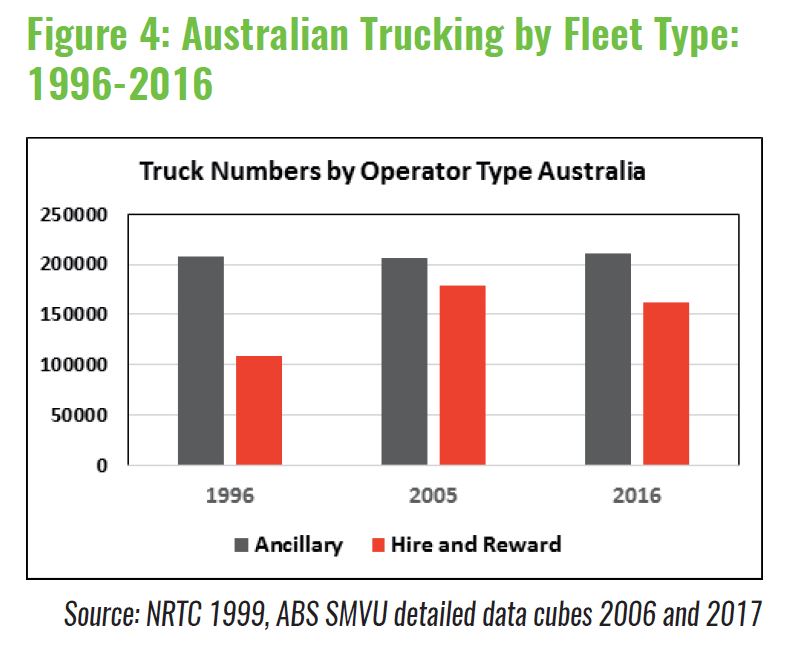

Hire and Reward Contribution to National GDP

The road transport sector comprises of more than the trucking sector. It also contains postal and courier operations, and public bus and coach operations. However, the total road freight sector is estimated to be 79 percent of the road transport GDP figure.

With the rise in public transport over the last 25 years the actual road freight component of road GDP will be smaller than that presented in figure 5 but even though the behaviour will track below this line the actual index will exhibit similar behaviours.

With the rise in public transport over the last 25 years the actual road freight component of road GDP will be smaller than that presented in figure 5 but even though the behaviour will track below this line the actual index will exhibit similar behaviours.

The June 1991/92 base year saw the road transport contribution to Australian GDP as $10,255 million dollars.

This grew by the end of the 2016/17 financial year to $23,856 million dollars. This reflected a compound per annum growth rate of 3.4 per cent per annum.

However, since June 2008, post the GFC, the road freight contribution to GDP not only stalled but went negative at -4.4 per cent below the June 2008 figure.

In fact, since June 2008, Australian road transport has been in a chronic depression at least for the H&R sector.

The road freight contribution is carried by the vehicles in the H&R sector and not by the entire commercial vehicle fleet.

The ancillary component of road transport GDP is not reflected in the national road GDP figure, but can be extracted from the national input-output tables. Few analysts have even undertaken this exercise.

However, a further indicator of the severe pressure in the H&R sector is that many configurations in the Australian road transport sector are performing less kilometres on average than they did a decade ago and forecast road pricing revenues are not coming to the road agencies.

This reflects the current efficient road pricing methodology that may not make State treasurers excited.

Diesel prices and registration fees: The ouch points in the industry

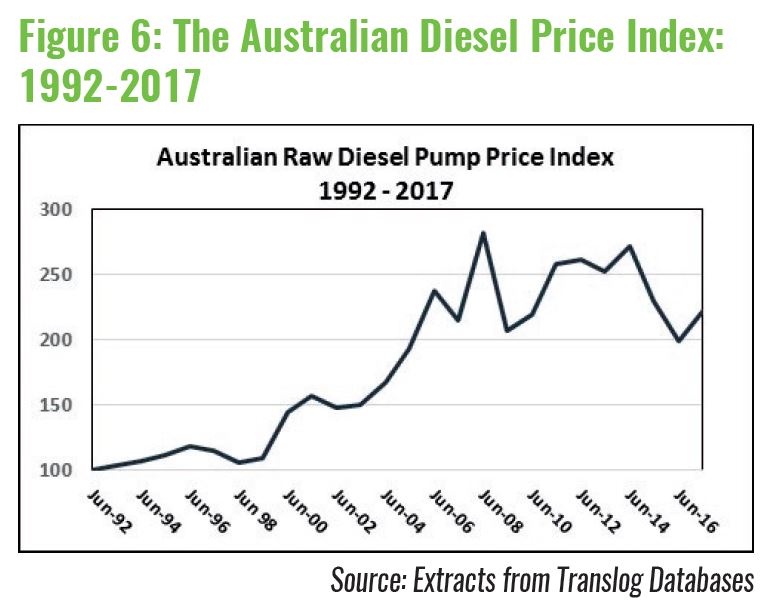

Over the last quarter of a century diesel fuel prices have fluctuated because of invasions and major global crises. Figure 6 reflects an index of raw Australian diesel prices averaged across raw pump and bulk drop prices. This index has not removed GST or the diesel fuel credit.

The index base of 100 starts in June 1992 and continues for the 25 years to June 2017. In June 2008, at the peak of the GFC oil prices hit a high of 281 index points.

This was a compound increase of 6.7 per cent per annum to June 2008. Since that time there has been an easing in fuel prices to 222 index points which has come as a relief to industry.

Over the full 25 years average annual compound growth was 3.24 per cent per annum but behaviour for this major cost input, has been less than well behaved, and has had operators often scrambling for fuel levies in their cost escalation negotiations.

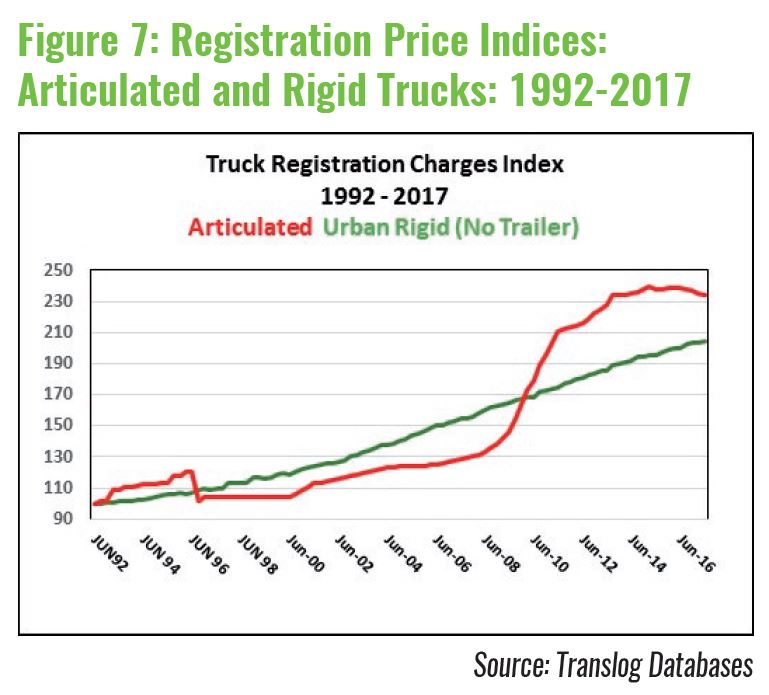

The second bugbear for operators are registration charges.

Changes in charges are a constant source of lobbying and examination of the appropriate use of the now evolved National Road Transport Commissions charges model that is still being refined and actively used in the Road Pricing Determinations.

Although the model can be argued as being equitable and efficient, as pricing should be, there have been some interesting variations in truck registration charges over the last 25 years.

Again, from a base of 100 in June 1992, the basket of articulated trucks saw an index growth rate of 3.46 per cent since June 1992 to June 2017.

However, since the GFC, or from June 2008, the articulated registration Index has grown by 6.49 per cent per annum to June 2017.

As road transport GDP went negative since June 2008 articulated trucks have experienced almost a 6.5 per cent increase per annum for each of the last nine years. This has been a pretty hefty slug to the industry.

On the other hand, rigid trucks not in combination, the backbone of e-commerce and many urban deliveries have experienced a steady 2.91 percent per annum average registration cost increase over the same 25 years, although heavy rigids in truck and dog combinations have had recent large increases.

In summary

Over the last quarter of a century road transport in Australia has experience long term growth even though there have been several significant hiccups along that road.

Growth in Gross tonne kilometres and tonnes carried have continued to grow at 3.3 per cent, and tonnes carried by 3.7 per cent per annum respectively.

Road transport GDP has gone negative since 2008 and in the face of this articulated registration charges have increased by 6.5 per cent per annum.

Also since the Global Financial Crisis ended, fuel prices have fallen which has been a relief, after surging to a 25 year peak at the height of the GFC in 2008.

The much unknown ancillary road transport sector is still an unknown sector of the industry. It contains more fleets and vehicles than its much examined ‘hire and reward’ counterpart that is often re-examined in detail especially in the fatigue and maintenance areas.

We know little of this side of the industry, this ancillary sector that has 3.5 times the fleets and 30 per cent more vehicles than those fleets thought of as ‘operators’.

In 25 years we only know how many vehicles in this sector and almost nothing about their safety, fatigue, maintenance or kilometre behaviour. Maybe this is a study for the next 25 years.

However, the ‘hire and reward’ operators are becoming more productive and inroads have been made with B-doubles, which have become the new workhorse in Australia, and the added benefits with the adoption of PBS vehicle configurations.

Both these vehicle classes have brought savings and safety benefits to the road freight sector.

How low would road transport GDP have actually fallen if the sector had been without these vehicles since the height of the GFC in June 2008?

The next 25 years will be an interesting story.

Can history teach us anything?

Do we believe Goethe when he said, “The only thing that history teaches us, is that history does not teach us anything!”

Perhaps he was not talking about road transport.